RAM Crisis: How the Shortage Affects IT Companies in 2026

Summary

Memory prices have surged 80-90% in Q1 2026 alone - and this time, the shortage is not cyclical. Driven by AI infrastructure demand, the global RAM crisis is reshaping costs, timelines, and procurement strategies across the IT industry.

In this article, you'll find out what's causing the shortage, who is affected and how, and what IT companies can do right now to adapt before the market stabilizes - which analysts don't expect before 2027.

The Global RAM Shortage in 2026: What’s Happening?

The global RAM market is facing a major price hike, with memory costs increasing by 80-90% in Q1 2026 so far compared to Q4 2025, reflecting a massive price increase in just a few months (from October - December 2025 to now) for which no one is prepared, neither IT businesses nor consumers.

DDR5 module prices have increased by over 35% compared to 2025, NAND flash has reached 25% with a prediction of reaching up to 40% by the end of 2026, and Enterprise NVMe SSDs are close to a 30-50% increase, all while global production capacity remains limited due to ongoing supply chain disruptions and delays in chip manufacturing.

Also worrying is the fact that analysts warn that the resulting deficit could persist for several years, perhaps until at least 2028. However, instead of panicking or waiting for things to change, my recommendation would be to adapt quickly and smartly to the new conditions in order to be able to withstand this period.

What is causing the RAM shortage?

The CNN reports that the RAM shortage is caused by manufacturers prioritizing demand for AI-powered data centers over consumer hardware.

And this time, the memory shortage cannot be treated as a temporary or cyclical challenge. It stems from fundamental changes in how the technology market and hardware demand operate. At its core, this is a structural shift in demand.

“The RAM shortage is more structural. This is really an AI-driven memory demand shock.”

- Matteo Rinaldi, Professor of Electrical and Computer Engineering at Northeastern University and the director of Northeastern University’s Institute for NanoSystems Innovation

According to Matteo Rinaldi, the demand for memory is growing permanently, not just temporarily, the main reason for which was the explosion of artificial intelligence (LLMs, training models, data centers, GPUs), and which manifests itself differently from the temporary shortage of chips that the markets experienced during the Covid-19 pandemic.

What the professor of electrical and computer engineering wants to convey is that the current memory production infrastructure was not built for this level of demand and, even if production increases, demand could continue to grow faster, leaving the problem of memory availability unresolved.

So… how exactly is AI involved?

AI models, especially large language models (LLMs) and generative AI systems, are fundamentally different from traditional software workloads:

-

Massive model sizes - Modern AI models contain billions or trillions of parameters, requiring enormous memory just to store the model and intermediate computations.

-

High-performance compute clusters - Training these models requires thousands of GPUs or AI accelerators, each consuming tens of gigabytes of high-speed memory (DRAM and HBM).

-

Constant data flow - AI training and inference rely on continuous access to large datasets, which also need to be held in memory to maintain speed and efficiency.

-

Infrastructure scaling - Cloud providers and AI-focused data centers are expanding rapidly, consuming a growing share of the global memory supply, leaving less available for traditional PCs, servers, and enterprise IT.

Unlike a consumer device, an AI data center is orders of magnitude more memory-hungry and far less forgiving about performance.

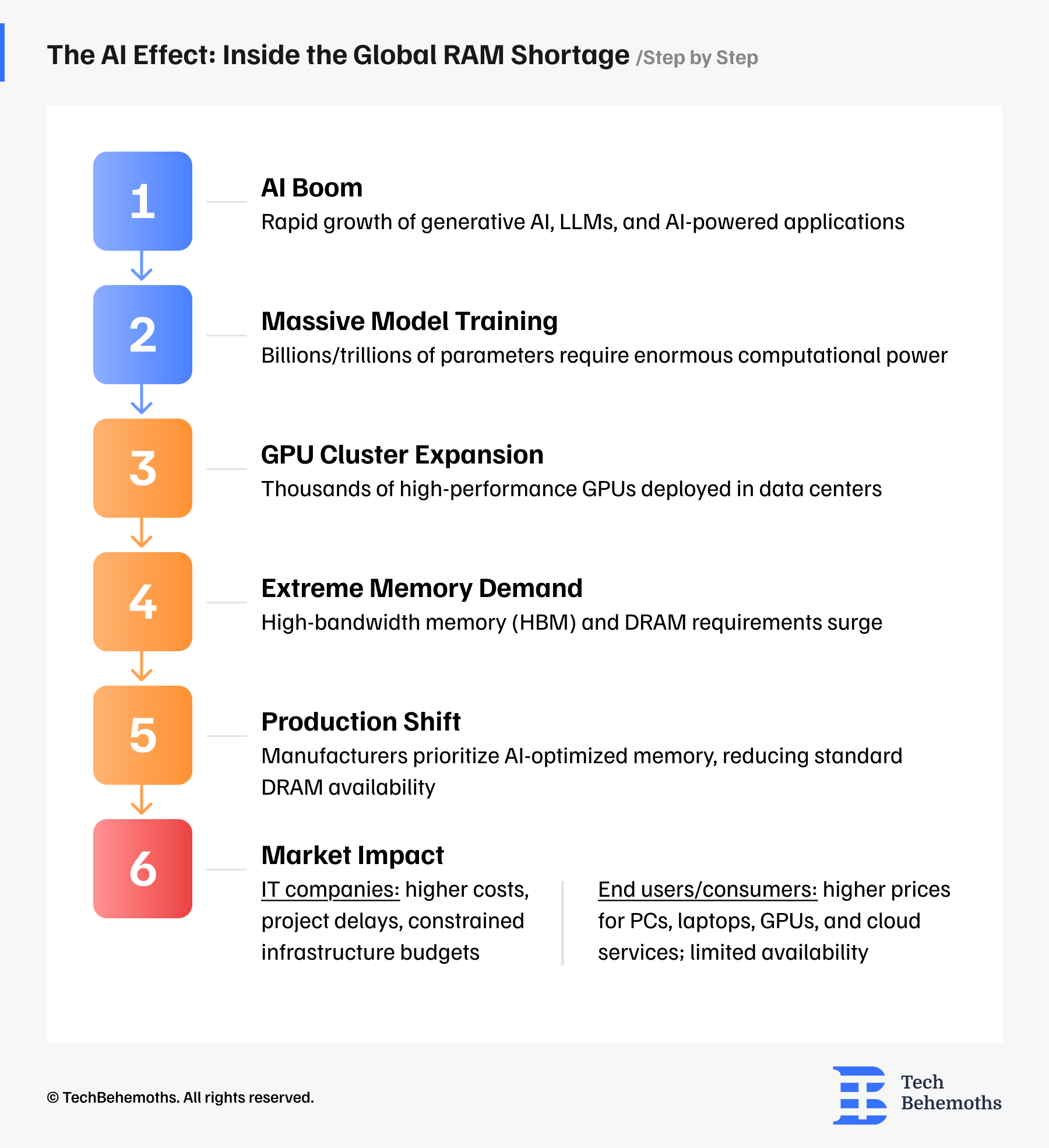

Once it is clear that AI is not just adding a small additional memory demand, but is working as a catalyst at the current time, redefining the basic memory requirements for the entire industry, let's see in the infographic below what the stages of evolution of the memory crisis are and who is affected by the consequences.

As represented in the roadmap-type infographic above, the global RAM shortage resulted from a clear sequence of events. The crisis started with the rapid growth of generative AI and LLMs, which fueled massive model training.

This fact requires thousands of high-performance GPUs, which consequently creates extreme demand for high-bandwidth memory (HBM) and DRAM, leading manufacturers to prioritize AI-optimized memory. As a result, standard DRAM supply for conventional IT infrastructure is constrained, causing higher costs, project delays, and budget reallocation for IT companies, while end users face higher prices, limited availability of PCs, laptops, GPUs, and increased cloud service costs.

Who is Affected by Memory Crisis

The industry changes resulting from the memory crisis of the past year will be felt and suffered especially by:

-

IT companies that produce hardware

-

PC and smartphone manufacturers

-

Hardware startups

-

End consumers (higher prices for devices)

Of course, there are also beneficiaries of the fluctuations generated by the memory crisis, and these are:

-

Memory chip manufacturers (e.g., Samsung Electronics, SK Hynix, Micron Technology)

-

Companies with existing Inventory (e.g., Dell Technologies, HP Inc., Lenovo)

-

Cloud & AI Giants (e.g., Amazon, Microsoft, Alphabet (Google), NVIDIA)

Who Benefits from the Memory Crisis

|

Category |

Examples |

How They Win |

|---|---|---|

|

Memory Chip Manufacturers |

Samsung Electronics, SK Hynix, Micron Technology |

Dominate the global market; can raise prices; prioritize production for the most profitable segments (e.g., AI, HBM) |

|

Companies with Existing Inventory |

Dell Technologies, HP Inc., Lenovo |

Can continue producing hardware without being affected by price spikes; achieve higher margins than competitors |

|

Cloud & AI Giants |

Amazon, Microsoft, Alphabet (Google), NVIDIA |

Long-term contracts with memory producers; secure memory supply; can pass costs to clients if needed |

SK Hynix ended 2025 with annual operating profits of ₩47.2 trillion (~$33.3 billion), and quarterly profits increased by about 137% compared to the previous period. Samsung was not far behind - its memory division generated operating profits of about ₩24.9 trillion (~$17.4 billion) for the entire fiscal year 2025, supported by solid market prices.

Another relevant example is Micron Technology: in the first quarter of fiscal 2026, the company reported revenues of $13.6 billion, with net income nearly tripling compared to the same period of the previous year.

This trend is also confirmed by analysts. According to XTB, gross margins for memory manufacturers are projected to reach approximately 69% in Q2 2026, with operating margins at 62% - with Seeking Alpha noting possible upside into the mid-70% range throughout the year.

On the other side of the supply chain, the pressure is felt differently. While it is difficult to isolate the direct financial impact of the memory shortage, available analysis shows that OEMs are being hit hard: high memory costs are eroding gross margins, as memory takes up a growing share of the BOM (bill of materials). Dell has felt the impact, as has HP, which forecasts gross margin declines driven by component prices - even as enterprise orders continue to grow. Importantly, OEMs with their own component inventories can better absorb these price increases than those without, making inventory management a real competitive advantage.

Finally, the big picture is rounded out by hyperscalers and AI companies, who, while not reporting strictly memory-related profits separately - these are typically included in cloud or AI revenues - are investing at a massive scale. Projected spending on AI infrastructure in 2026 exceeds $630 billion globally, indirectly fueling memory demand and thereby supporting the entire ecosystem.

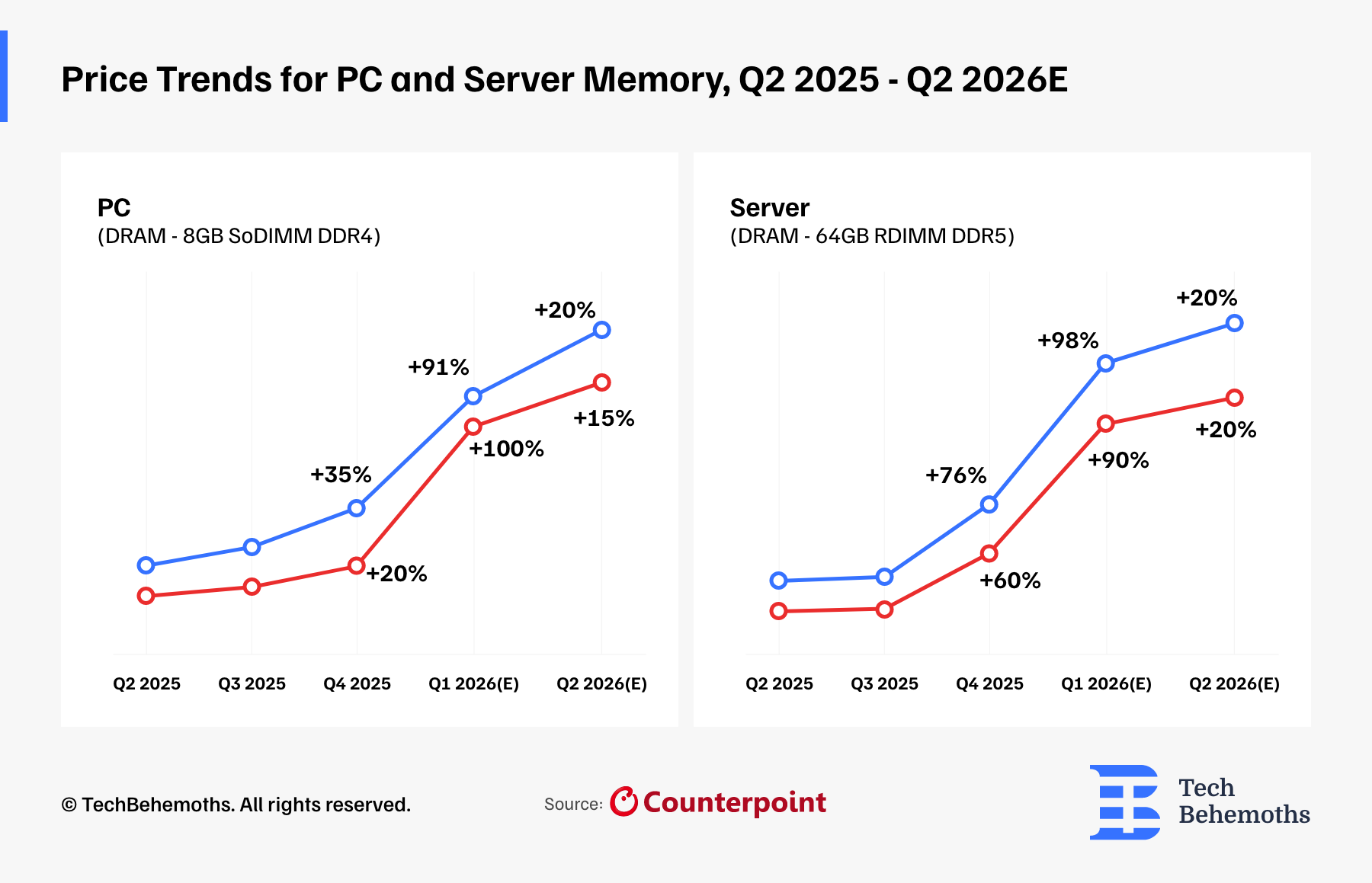

The chart above, drawn up by Counterpoint Research, tracks the evolution of prices for two memory categories - PC and Server - across two component types: DRAM (black line) and NAND (red line), between Q2 2025 and Q2 2026E (estimated).

According to Counterpoint Research's Memory Price Tracker, both PC and server memory segments recorded dramatic price surges between Q2 2025 and Q1 2026.

PC Memory

The PC segment shows a clear acceleration in the second half of the range:

-

DRAM (8GB SoDIMM DDR4) has grown progressively: +35% in Q3, +91% in Q4 2025, reaching an estimated +20% in Q2 2026 - meaning that the price has stabilized at an already high level, not fallen.

-

NAND (1TB NVMe DRAM-less) has seen a dramatic jump of +100% in Q4 2025, followed by a moderation to +15% in Q2 2026E. This sudden spike confirms that NAND, previously relatively quiet, exploded in Q4-Q1.

Server Memory

The server segment shows even more pressure, which is consistent with the data from the source:

-

DRAM (64GB RDIMM DDR5) grew by +76% in Q3, with a massive jump of +98% in Q1 2026E - the largest jump visible in the chart. The source confirms that the fixed contract price has gone from ~$450 in Q4 2025 to over $900 in Q1 2026, with the prospect of exceeding $1,000 in Q2.

-

NAND (3.84TB NVMe) grew by +60% in Q3, then +90% in Q1 2026E, with an estimated stabilization at +20% in Q2.

The Q2 2026 estimates suggest a slowdown in the rate of increase, with prices plateauing at record highs - a level that, as Counterpoint analysts note, may well represent the new normal for the memory market going forward.

“The memory profitability is expected to reach unprecedented levels. DRAM operating margins have already reached the 60% range in Q4 2025, marking the first time margins for general-purpose DRAM have surpassed those of HBM. The first quarter of 2026 is set to be the period where DRAM margins exceed their historical peaks for the first time. Having said that, this will either set a new normal or a very high bar which looks solid now but could make the next down cycle (if there is one) look uglier.”

- Jeongku Choi, Senior Research Analyst at Counterpoint Research

How the RAM Shortage Impacts IT Companies

The global RAM shortage, driven by AI infrastructure demand, is creating structural challenges for IT companies:

-

Higher Costs

DRAM and NAND prices have surged as manufacturers prioritize memory for AI servers and data centers.

-

Limited Supply

Standard memory for servers, workstations, and cloud infrastructure is constrained, slowing hardware procurement.

-

Project Delays

IT deployments, upgrades, and cloud expansions may be postponed due to memory scarcity.

-

Budget Reallocation

Companies must prioritize memory purchases, reducing spend on other strategic areas.

-

Competitive Differences

Large IT firms with supply agreements are less affected, while smaller vendors face stronger disruption.

What is RAM and Why Is It Critical for IT Businesses?

RAM (Random Access Memory) is the short-term memory of a computer that stores data currently used by applications and operating systems. It allows servers, development environments, and cloud systems to process tasks quickly.

IT companies rely on large amounts of RAM for software development, virtualization, databases, and AI workloads.

When RAM is limited or expensive, system performance drops and infrastructure costs increase.

The results of IDC’s market analysis have confirmed that the 2026 memory shortage is a structural phenomenon rather than a normal cyclical event, meaning IT companies must adapt to a market where memory is scarcer and more expensive throughout 2026 and potentially into 2027-2028.

It will also inevitably force adjustments in hardware planning, budgets, and project timelines, affecting small to medium IT businesses directly and, as a result, the ordinary (final) consumers indirectly.

|

Stakeholder |

Impact Area |

Effect |

Timeframe |

Severity - Business Implication |

|---|---|---|---|---|

|

IT Companies |

Infrastructure costs |

Higher DRAM/RAM prices increase server, workstation, and GPU costs. |

Short-Medium (2026-2027) |

High - direct effect on CAPEX and operating budgets |

|

Project timelines |

Limited memory availability delays software development, product launches, and cloud expansions. |

Short (2026) |

Medium - affects go-to-market and delivery schedules |

|

|

Budget allocation |

Companies must prioritize memory purchases, potentially reducing other strategic investments. |

Medium (2026-2027) |

Medium - strategic trade-offs across projects |

|

|

End Users (consumers) |

Device pricing |

Increased RAM costs are passed to PCs, laptops, and GPUs. |

Short (2026) |

Medium - higher purchase cost for end-users |

|

Hardware availability |

High-memory devices (gaming PCs, AI workstations, servers) are harder to source. |

Short-Medium (2026-2027) |

Medium - supply constraints impact adoption |

|

|

Cloud service costs |

Cloud providers incur higher infrastructure costs, potentially increasing fees for AI, gaming, and design workloads. |

Medium (2026-2028) |

High - indirect but significant for business and consumer users |

RAM Shortage Affected Industries

The RAM shortage does not hit all sectors/industries equally. Its impact depends on how memory-intensive the business is, how much pricing power it has, and whether it secured supply agreements in advance.

PC and laptop manufacturers are among the hardest hit. Memory now accounts for approximately 20% of a laptop's hardware cost - up from 10-18% in the first half of 2025. HP disclosed in its Q1 2026 earnings call that memory now represents 35% of a PC's bill of materials, up from 15-18% the previous quarter. Lenovo, Dell, HP, Acer, and ASUS have all warned customers about price increases of 15-20% and contract resets as a direct response to the shortage.

“The sub-$500 entry-level PC segment will disappear by 2028.”

- Ranjit Atwal, Sr Director Analyst at Gartner

Entry-level PCs under $500 may effectively disappear from the market by 2028, according to Gartner, which also estimates average PC prices will rise by approximately 17% overall.

Smartphone manufacturers, particularly those operating in the mid-range and budget segments, face an especially difficult position. Entry-level and mid-range manufacturers - TCL, Transsion, Realme, Xiaomi, Oppo - operate on thin margins and have little choice but to pass costs to consumers. Apple and Samsung are relatively better protected due to 12–24 month supply agreements. The cruel irony is that just as the industry needs more memory to support AI PCs - Copilot+ requires a minimum of 16GB, that memory has become prohibitively expensive, creating a perfect collision between demand and crisis.

SMBs with on-premises infrastructure are arguably the most vulnerable category. Unlike large enterprises with dedicated procurement teams and volume contracts, small and medium businesses have neither the leverage nor the cash reserves to navigate sudden price spikes. A Dell PowerEdge R750 server with 256GB RAM cost approximately €8,000 in 2024, and the same server now costs between €11,000 and €12,000, which is a 40–50% increase. Delivery times have extended from 2-3 weeks to 6-8 weeks, with SMBs consistently last in line compared to larger customers.

Game development studios and gaming hardware are also feeling the pressure. NVIDIA CEO Jensen Huang was directly asked at CES 2026 whether gaming customers would resent AI technology because of rising GPU and console prices driven by the memory shortage. Graphics cards and gaming PCs require significant DRAM, and as manufacturers prioritize AI-optimized memory, consumer GPU configurations are becoming more expensive and harder to source.

Consumer electronics beyond computing - including automotive, smart TVs, and IoT appliances - face a secondary wave of impact. The shortage is extending beyond computing, affecting automotive, television, and consumer electronics sectors as memory manufacturers have reduced or halted production of legacy chips used in these devices.

SaaS platforms and data-intensive companies face a less visible but equally real impact: rising cloud infrastructure costs. As cloud providers absorb higher memory expenses, those costs are gradually passed on through pricing adjustments, directly affecting SaaS businesses that rely on elastic cloud infrastructure to scale.

Turning the RAM Crisis into Opportunity: IT Strategies That Work

The companies responding most effectively are those treating this as a structural shift, not a temporary disruption.

Cloud migration is the most immediate strategy for SMBs - it eliminates the need to purchase physical servers at inflated prices and transfers procurement burden to hyperscalers with secured supply. Architecture optimization follows closely: engineering teams are redesigning systems using caching, lazy loading, data compression, and optimized database queries to reduce raw memory requirements. VMware Cloud Foundation 9.0's new memory tiering features offer a concrete tool for this.

Strategic procurement timing matters more than ever - H1 2026 represents peak pricing risk, so non-urgent deployments are best delayed toward H2. Companies are also diversifying supply chains, turning to authorized independent distributors to fill gaps where traditional vendor allocations are blocked. Those that relied on a single supplier are the most exposed.

"The best approach right now is using data — not panic — to drive device refresh decisions."

- Ian Murray, Director, Device Lifecycle Strategy, Insight

|

Action |

What IT companies should do |

Horizon |

Impact |

|---|---|---|---|

|

IMMEDIATE ACTIONS |

|||

|

Migrate to cloud AWS, Azure, GCP |

Avoid physical server purchases at +40–50% prices; leverage hyperscaler supply agreements |

Now |

Cost & supply |

|

Audit memory usage Internal infrastructure |

Most environments run at 40-60% utilization - consolidate before buying new hardware |

Now |

Cost reduction |

|

Diversify suppliers Procurement |

Add authorized independent distributors; single-vendor dependency = highest exposure risk |

Now |

Supply continuity |

|

MEDIUM-TERM STRATEGIES |

|||

|

Optimize architecture Engineering |

Implement caching, lazy loading, data compression; reduce raw memory dependency at software level |

Q2-Q3 2026 |

Long-term savings |

|

Lock in pricing Contracts |

Negotiate fixed-price agreements now; spot prices are at historic peaks in H1 2026 |

Q2 2026 |

Budget stability |

|

Delay non-urgent upgrades Hardware planning |

H1 2026 = peak pricing window; push discretionary hardware purchases to H2 or 2027 |

H2 2026 |

Cost avoidance |

|

STRATEGIC DECISIONS |

|||

|

Reassess on-prem vs. cloud IT leadership |

Server costs up 40-50% - cloud-first is now financially stronger for most SMBs |

2026 to 2027 |

Infrastructure model |

|

Plan with multi-year horizon Budget & roadmap |

New fab capacity arrives 2027–2028; budget for sustained high prices, not a quick recovery |

2026 to 2028 |

Financial resilience |

|

Outsource infrastructure MSPs & colocation |

Providers that locked in hardware pre-shortage offer competitive rates vs. in-house procurement today |

Ongoing |

Cost & flexibility |

What to Expect Next

What is 100% clear is that relief is unlikely before 2027. To make some points about the current context and where this is going, I would like to highlight once again that TrendForce called the 50-55% quarterly price increase in the first quarter of 2026 "unprecedented", and Jeongku Choi of Counterpoint Research warned that DRAM margins exceeding historical peaks could either "establish a new normal or make the next down cycle look uglier".

Find IT Managed Services Providers

Connect with trusted IT Managed Services companies to reduce infrastructure costs and tackle the 2026 memory shortage.

On the supply side, Micron is building two fabs in Boise, Idaho, expected to be operational in 2027-2028, and another in Clay, New York, planned for 2030. Building a new DRAM fab requires $10-20B and 2-3 years, meaning no announced capacity will arrive before 2027. Samsung and SK Hynix began HBM4 mass production in February 2026, with Samsung planning a 50% HBM capacity increase this year.

Also worth mentioning is that DDR6 is in active development but will reach commercial availability in 2027-2028, initially reserved for enterprise and AI use.

Partial price normalization is realistic from 2027 onward, with a potential oversupply scenario in 2028-2029 if AI demand moderates. IDC confirmed this is a structural phenomenon, not a cyclical one, which is why companies that adapt now through diversified supply, optimized architecture, and multi-year procurement planning will be best positioned when the market stabilizes.

Final Word

The memory shortage of 2026 marks a turning point, not a temporary setback.

The data is unambiguous: prices have doubled in a single quarter, relief is unlikely before 2027, and the structural forces driving demand - AI infrastructure, LLM expansion, data center scaling - show no signs of slowing. For IT companies, this means that waiting for the market to normalize is itself a strategic risk.

The window to act is now - before H2 pricing peaks, before project timelines slip further, and before procurement options narrow. Those who treat this as a structural shift, rather than a cyclical inconvenience, will navigate it with far greater resilience.

The new normal is here, and the only question is how quickly you adapt to it.

Related Questions & Answers

Why are RAM prices so high in 2026?

Will RAM prices drop anytime soon?

How can a memory shortage affect my IT budget?

Should I buy hardware now or wait?

Is cloud a better option right now?

How long will this last?

I tend to create digital content that captures, inspires, and generates impact. I resonate with the idea that less is more. My approach combines strategy, creativity, and analysis to build authentic and relevant messages. Beyond the digital space, nature is my sanctuary - a place of inspiration and balance. Exploring landscapes, I find clarity in nature's simple beauty.

Discover more TechBehemoths Insights

Learn practical tips and insights about IT Companies, how to find the right company for your projects.

Read the latest news about Market Trends and fresh Interviews.